JetBlue & Spirit Target Florida with New Fort Lauderdale Routes

JetBlue adds new routes and Mint service in Fort Lauderdale, while Spirit launches Key West flights. See what’s changing for Florida flyers.

Alaska Airlines launches Seattle to Reykjavik service on the 737 MAX 8. Here’s why this uncontested route may be their smartest international move yet.

Beginning May 28th, 2026, Alaska Airlines officially enters the transatlantic narrowbody market, launching service between Seattle-Tacoma International Airport and Reykjavik’s Keflavik International Airport. Alaska joins United, American,Delta, and JetBlue as U.S. carriers operating single-aisle aircraft on routes that have historically demanded widebody jets.

Alaska will be using the Boeing 737 MAX 8. This will be the longest transatlantic route operated by a U.S. carrier on a 737 MAX, and it’s a meaningful statement against United, who also uses the Boeing 737 Max on transatlantic flights to Europe.

Ironically, this route rollout has been overshadowed by Alaska’s recent commencement of widebody 787 Dreamliner service between Seattle and Rome a few weeks ago. Based on our analysis there is no question that the Iceland route is arguably the smarter near-term business decision of the two.

So why now? Is Alaska positioning itself to compete in the narrowbody transatlantic space? How is Seattle competitor Delta responding? And will this route be successful? Let’s dig in.

Just over a year ago, we covered Alaska’s first international related announcements. They onboarded 787 Dreamliners from Hawaiian, announced service between Seattle to Rome, with a London route waiting in the wings.

Tucked inside a September press release that barely made a ripple…Alaska said it was going to begin offering seasonal 737 MAX 8 service between Seattle and Reykjavik, starting May 28th, 2026.

The quieter announcement/route pairing may actually be the more strategically sound one, compared to their Seattle-Rome route.

Alaska already had the 737 MAX 8 in its fleet. No new aircraft type to operate to Iceland. No need to ingest an operating airline and grab planes from their fleet like Alaska did with Hawaiian.

Also, Alaska had already secured a codeshare agreement with Icelandair. This codeshare functions as a driver of passenger traffic, additional source of revenue and a safety net, in regards to flights between Seattle and Reykjavik.

Icelandair already flies year-round service to Iceland from Seattle. Alaska is going to be running seasonal flights during peak demand and funnels off-season passengers to Icelandair, collecting revenue on those seats regardless.

There is currently no U.S. carrier competition on the SEA-KEF route pairing. Alaska’s only theoretical direct competitor was Icelandair but they’re partners. The road ahead is about as clear as it gets for a new international route launch.

Compare this to Alaska’s Rome route, and the risk profile looks completely different. Rome is a leisure-heavy destination with no proven Alaska brand awareness in that market, operated on a newly acquired widebody that required significant initial investment in the form of buying an existing airline.

Iceland, by contrast, is a proven leisure destination by Icelandair from Seattle, served on planes already existing in Alaska’s fleet, with a codeshare partner absorbing the off-season risk. Of Alaska’s current international rollout, this is the one with the floor underneath it.

Alaska’s timing reflects both opportunity and a broader industry trend. Legacy carriers historically operated long, thin transatlantic routes on Boeing 757s before pulling back as the fleet aged.

Now United and American have revitalized their narrowbody transatlantic product with their Boeing 737 Maxes and Airbus A321XLR additions. JetBlue has been running flights across the pond for several years. Alaska isn’t following that trend for trend’s sake but they’re filling a specific market gap opportunity that has been ripe for the taking on the West Coast.

Delta and United both operate seasonal service to Iceland, but exclusively from East Coast hubs. The entire Pacific Northwest has been left to Icelandair alone, which also serves Portland in addition to Seattle.

Alaska’s West Coast network is one of the strongest domestic feeder systems in the country, giving it a meaningful structural advantage in driving demand into Seattle for their own rendition of the SEA – KEF route.

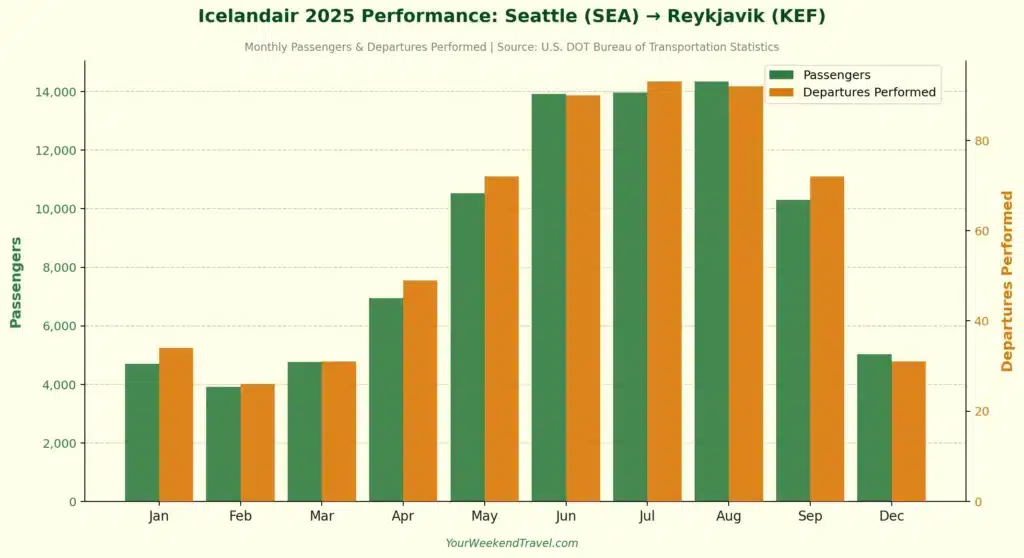

BTS data backs up the planned timing of the rollout for Alaska. Last year, Icelandair concentrated the majority of its SEA-KEF departures between May and September, with July and August representing peak operations. Alaska is launching directly into that window, chasing the demand curve rather than testing it.

More clear runway for Alaska to takeoff and be successful on this route pairing.

Delta is Alaska’s most formidable competitor at SEA-TAC, and they’ve shown a willingness to respond aggressively when Alaska moves into markets they care about like Rome and Asia being recent examples. But Iceland? Delta barely blinked.

That’s the correct call. Here’s why.

Delta has publicly committed to not deploy narrowbodies on transatlantic routes, simply because they cannot replicate their widebody premium product on narrowbodies. Their Iceland operation reflects this philosophy since they’re mostly using the Boeing 767-300 while sprinkling in some aging 757-200s.

| Departure Airport | Departures Performed | Scheduled Seats | Total Passengers Flown | Load Factors | Aircraft Used |

| DTW | 119 | 23100 | 18763 | 81.22% | 757-200,767-300 |

| JFK | 203 | 42918 | 36248 | 84.45% | 767-300 |

| MSP | 108 | 21040 | 18103 | 86.04% | 757-200,767-300 |

| Total | 430 | 87058 | 73114 | 83.98% |

Source: U.S. DOT Bureau of Transportation Statistics, 2025

Delta ran 430 total departures to Iceland across three hubs in 2025, with load factors consistently above 81%. They’re operating efficiently, generating solid yields, and have no reason to disrupt that with a speculative West Coast expansion.

Deploying a widebody on a relatively thin SEA-KEF route would cannibalize their own load factors and potentially dilute margins across the broader company picture. Committing their widebodies on higher-yield long-haul routes is simply better capital/equipment allocation.

Delta isn’t losing sleep over Alaska’s Iceland service. And they probably shouldn’t be.

Alaska’s Pacific Northwest fortress is largely insulated from traditional competition on this route. The real area of risk exposure is likely indirect, like premium loyalty travelers in the PNW who might connect east to use Delta or United metal on flights to Iceland. That’s a real but narrow slice of the market, and it only applies during peak season when those carriers are operating anyway.

The long-game question is whether any low-cost or emerging carriers make a move on Iceland from the East Coast. Two names are worth watching.

Southwest Airlines filed for DOT authorization to conduct overseas operations over a year ago and has done nothing publicly with it since. But the intention is there.

Southwest is committed to going premium. They are building lounges, enhancing cabin configurations,which is a clear pivot toward the higher-margin leisure traveler.

Iceland as a destination fits well for that customer profile. Southwest already has an interline agreement with Icelandair in place, which basically mirrors the structure Alaska used to de-risk their own entry. A Baltimore-based seasonal operation with Icelandair overflow during the off-season is entirely plausible.

Breeze Airways is a longer shot, but worth noting. The airline recently went international for the first time with Caribbean service and filed its own DOT transatlantic authorization. Breeze founder David Neeleman has specifically pointed toward Ireland and the British Isles as potential targets for seasonal transatlantic operations. Iceland fits squarely within that geographic and commercial logic.

Critically, neither of these scenarios threatens Alaska’s SEA-KEF position. Both Southwest and Breeze are East Coast-oriented airlines. If they do enter the Iceland market, they’d be competing with Icelandair, Delta and United not Alaska.

Alaska’s Iceland service isn’t a reaction to what United, American, and JetBlue are doing in the transatlantic narrowbody space. It’s a calculated move on an uncontested route, enabled by the right aircraft, the right partner, and the right timing.

The Icelandair codeshare is the structural backbone of this entire strategy. It removes the most significant downside risk. The launch timing helps Alaska to capture full passenger loads during peak summer demand. No U.S. carrier is going to challenge them out of Seattle on this route in the near term.

The one real vulnerability is premium loyalty leakage. PNW travelers with status on Delta or United who choose to connect east rather than fly Alaska. It’s a real issue, but a manageable one given the convenience premium Alaska holds for Seattle-origin passengers.

Expect strong margins on this route. The ceiling is high, the floor is protected, and the competition isn’t coming.